Why the CPP now has a $500 billion surplus

Over the past fifteen years, CPP Investments has been one of the most successful pension fund investors in the world. As a result, the assets of the CPP have grown far beyond the levels projected in earlier actuarial reports.

In 2010, according to the Chief Actuary’s 25th Actuarial Report, the CPP fund stood at approximately $134 billion. At that time, the plan was considered fully funded under the actuarial framework, meaning that if the fund earned an average investment return of about 6% per year (the blue box below), it would be sufficient—together with future contributions—to sustain CPP benefits for the next 75 years.

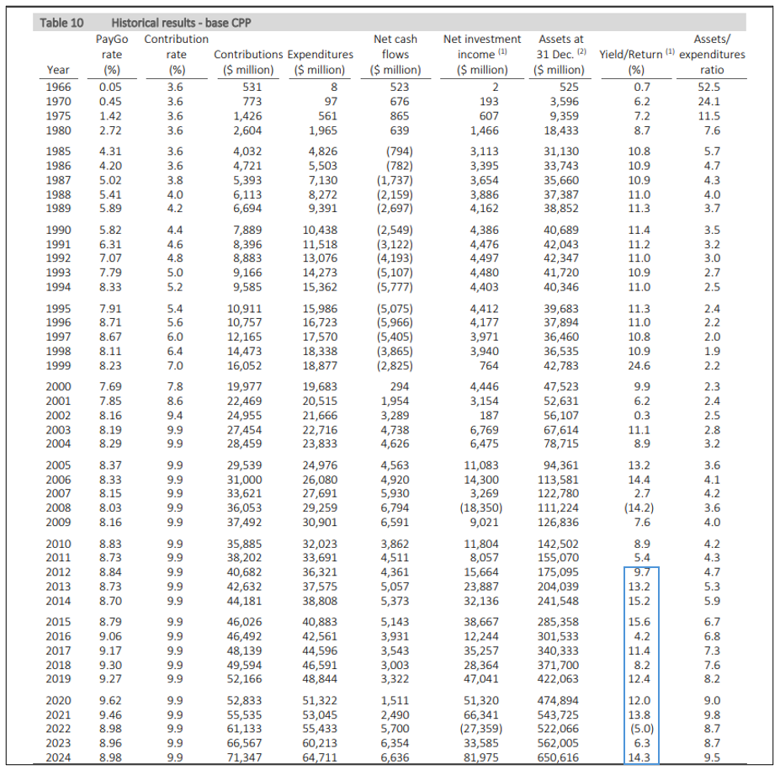

Since 2012, our Chief Actuary’s target of roughly 6% per year was exceeded by 4%, on average, as shown below, taken from Table 10 of the most recent actuarial report - the 32nd

Averaging the returns from 2012 to 2024 and including the 10.8% return for 2025 yields a 10.2% return for the last 14 years. The 2010 report suggested that, for long-term stability, the fund would need $366 billion by December 31, 2025, as shown in the red box.

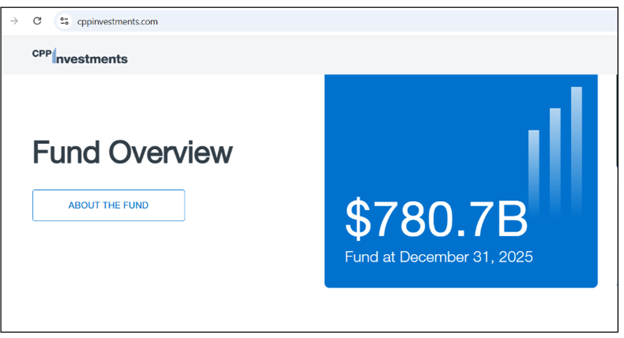

However, the actual outcome has been dramatically different. According to the CPP Investments website, the fund reached $781 billion on December 31, 2025—more than double the level projected in the earlier actuarial scenario. The fund is now two funds - the comparable Base CPP fund ($732 billion today) and the Additional CPP Fund created in 2019, and accumulating its own surplus. The comparable base fund is now exactly double the amount our Chief specified is needed to fund all CPP pensions for 75 years.

What has differed substantially from earlier projections is the investment performance of CPP Investments.

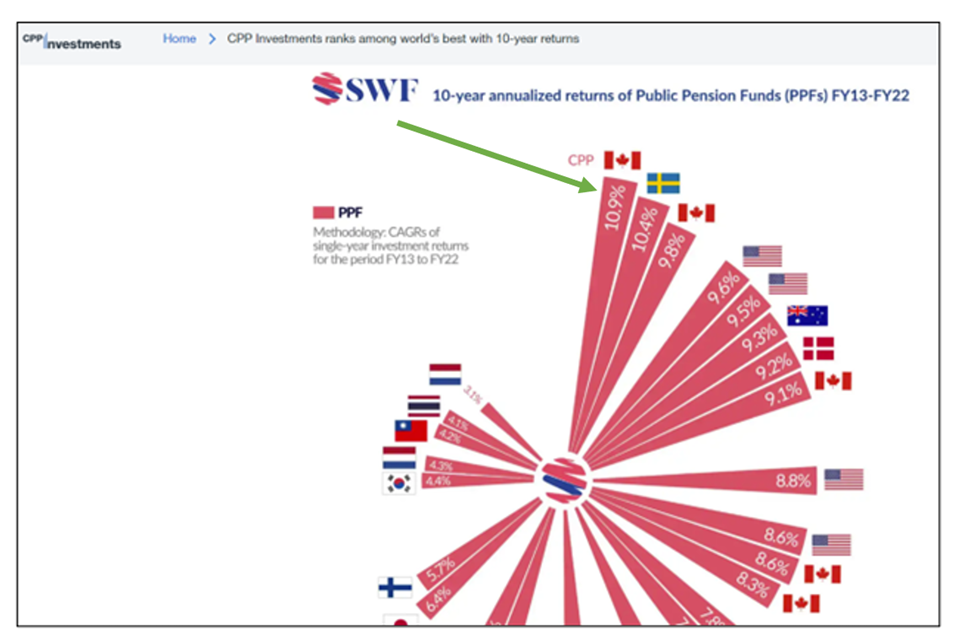

For the past fifteen years, CPP Investments has achieved an average return of roughly 10% per year. Independent pension industry research supports this strong performance. According to Global SWF, a New York–based sovereign wealth and pension fund research organization, CPP Investments ranked first among 300 major pension funds worldwide for the ten-year period ending in 2022, with an average annual return of 10.9%.

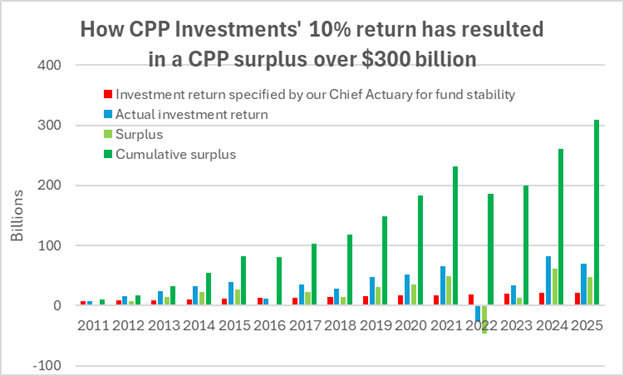

The chart below, based on Table 10 of the Chief Actuary’s 32nd Actuarial Report, illustrates how the CPP fund has grown far beyond the levels anticipated in earlier projections.

CPP Investments has several structural advantages that allow it to pursue higher long-term returns than many institutional investors. These include its very long investment horizon, its global diversification, and its large exposure to private markets. For example, the fund’s private equity portfolio—approximately one-third of total assets—reported a 34% return in 2022, according to the CPP Investments 2022 Annual Report on page 43.

Consider Ontario’s 407-ETR, a privately operated toll highway. CPP Investments owns approximately 44% of the company that operates the road, making it one of the largest shareholders.

The Pennsylvania Turnpike is frequently described as the most expensive toll road in the world. It charges roughly 27.4 cents CDN per kilometre. In contrast, tolls on the 407-ETR can reach as high as $1.20 CDN per kilometre, which is over four times higher.

Despite these higher tolls, the highway is widely used because it can significantly reduce travel time for commuters in the Greater Toronto Area. For thousands of drivers per day, the time savings outweigh the higher cost.

CPP Investments has also indicated publicly that it expects a 13% return per year for the next two years. In the image below, taken from the Globe and Mail on March 7, 2026, CPP Investments anticipates increasing the fund from $781 billion in 2026 to $1 trillion by 2028.

For the $781 billion fund to reach $1 trillion in value by 2028, after accounting for net contributions, the fund would need a 10% return, not the Chief Actuary’s recommended 6% return. This means CPP Investments predicts the fund will add roughly $80 billion more to the current $500 billion surplus by 2028.

By forecasting using the average return of the last 15 years (as pension experts recommend), the amount needed to meet all CPP pension commitments becomes much less. The fund only needs to be $250 billion in size, presuming an ongoign 10% return. This means our CPP fund is closer to 300% funded, with a $500 billion surplus.

The Asset/Expenditure Ratio further confirms our CPP fund has a huge surplus. It is the ratio of assets at the end of one year to the expenditures (pensions paid) in the next year. A larger ratio means the fund is better funded. In his 2010 25th Actuarial Report, on page 10, our Chief Actuary stated,

“The ratio of assets to the following year’s expenditures is projected to grow from 3.9 in 2010 to 4.7 by 2020 and 5.2 by 2050.”

On January 1, 2026, the assets of the comparable Base CPP fund were $732 billion. The recent 32nd Actuarial Report, Table 11, predicts expenditures will be $72 billion. This means the Asset/Expenditure ratio in 2026 is 10.2. A $200 billion surplus distribution would reduce the ratio to 7.4, still much higher than our Chief Actuary’s target of 4.78 for 2026.

Even after a $200 billion CPP surplus distribution, the CPP’s Asset/Expenditure ratio would still be 55% higher than our Chief Actuary’s target for 2026 and 42% above his target for 2050. Moreover, that prediction presumes a future 6% investment return when a 10% return is much more likely.

Outside Canada, the media tells the truth

The entire mainstream media, including “our” CBC, will not publish details of this massive windfall gain for Canadians and Canada. It finally took a respected international publication, The Economist, to write:

“Canada’s vast pension fund is gaining even more financial clout. The fund’s portfolio size has more than tripled over the past decade and is going to become only more gigantic.”

And since those words were published in January 2019, the fund has increased by another $400 billion.

The size of the surplus is enormous

To put the scale of these figures into perspective:

A $500 billion surplus means each CPP member has, on average, a $23,000 more in his CPP fund than is needed to fund his pension. And that is presuming future returns averaging 6%, not the likely 10%.

$500 billion is comparable to about $5 trillion in the United States on a relative scale.

$500 billion is approximately 18 times Canada’s average annual federal deficit (excluding pandemic years).

$500 billion is equivalent to 36% of Canada’s total federal debt.

In most pension systems, when assets substantially exceed the amount required to meet future obligations, a portion of the excess is distributed to members. A common benchmark in pension practice is that a surplus of roughly 25% above liabilities should trigger surplus sharing. The CPP’s 200% surplus is now eight times the 25% guideline, and mushrooming.

Without a surplus distribution, older pensioners will die never receiving their fair share of the surplus, even though it was created using their money. A surplus distribution addresses the principle of generational equity, the goal of all pension fund managers. One study found that those in the top quintile of income live 13 years longer than those in the bottom quintile. Since 2016, one million low-income seniors have died earlier than they should have, with a lower quality of life because they never received their deserved $10,000 from the CPP’s irrefutable $500 billion surplus.

Mysteriously, our Chief Actuary has refused to even acknowledge this $500 billion, 200%, surplus. He is very aware that, if the news of the CPP’s surplus and future potential becomes known, the need for other pension funds, and hence actuaries, will plummet. Details of why and how self-serving actuaries have abandoned Canadians and helped suppress the news of the CPP’s $500 billion surplus can be found here.

How you can help

As a professor, I received considerable income to work only seven months a year with the protection of tenure. Because Ryerson University matched my contributions towards my $110,000 pension, albeit indirectly, all Canadians paid for half my pension. I feel I owe Canadians and Canada. When I stumbled on this cover-up, combating it is my way of paying back.

I have spent roughly 10,000 unpaid hours trying to bring CPP justice to Canadians. If you agree with the above, on behalf of millions of struggling Canadians, hopefully you will spend a few minutes helping.

Because they were inundated with expressions of concern regarding Bill C-9, the Conservative Party participated in a prolonged filibuster. If enough Canadians similarly inundate politicians about their inaction regarding the CPP’s surplus and potential, we may finally enjoy CPP justice. On behalf of millions of struggling Canadians, I implore you to bombard our politicians with a message like this:

Dear Mr. Carney (or your MP),

Based on the website, www.fixthecpp.ca, the evidence is overwhelming that our CPP now has a $500 billion surplus which could be used to assist millions of struggling Canadians. A no-risk $200 billion CPP surplus distribution could lead to immense relief for the near-half of my fellow Canadians who are now within $200 of insolvency.

Moreover, by notifying young Canadians that a $100,000 CPP pension in 2026 dollars is likely, you could provide financial and emotional relief to Canada’s young who are struggling much more than older Canadians.

Your failure to exploit this opportunity is suspicious. I urge you to right the ship and bring these deserved benefits to Canadians.

Based on Town Hall Meetings, Albertans may separate because you refuse to treat the CPP using standard pension practice.

Sincerely,

Etc.

You may want to tone down the anger. There is no danger. I have sent more strongly worded emails to all MPs before. When one retired professor complains, it is easy to press Delete. If hundreds or thousands complain, it is not so easy.

In 2018, when I told CARP’s two female Vice-Presidents of Advocacy, a lawyer and an accountant, that two thirds of low-income seniors are women, they finally responded and acted against the 76% clawback.

Research shows that, in Canada’s financial industry:

Women only hold 30.8 % of senior management roles.

In finance and insurance, women hold about 26.7 % of board seats.

About 15–20 % of financial advisors in Canada are women.

Women earn around 82 cents for every dollar men earn,

For women under 65, they earn 78 cents for every dollar that men earn.

Probably men are predominantly orchestrating this cover-up. If you are a woman, I urge you to, like CARP’s two female advocates, stand up for women.

The only way to combat this cover-up is to notify all politicians that more and more Canadians are aware of this cover-up and their participation will be known by thousands or even millions.

Mr. Carney is the head of the snake. His email is mark.carney@parl.gc.ca. All other MPs can be found at www.ourcommons.ca/members/en/search.