Why the financial industry would lose billions, per year

When I discovered low-income seniors were subjected to a GIS clawback rate as high as 76%, I pleaded with CARP to advocate for changes. When I attended CARP’s press release meeting in 2018, their two Vice-Presidents of Advocacy proudly showed me their advocacy efforts to eliminate this vicious clawback. Finance Minister Morneau listened and, in his March 2019 Budget, he substantially eliminated the clawback. That was easy, I thought - a few emails to CARP demonstrating the injustice and then CARP advocated for change. This GIS legislation is now costing our government $440 million per year but it has had no impact on the profits of any Canadian industry.

At the meeting, when questions were asked, I gave a five minute summary of the CPP’s surplus, claiming every senior deserved $10,000 each, on average, from the CPP’s surplus. Overall, seniors would receive a deserved $60 billion. Because standard pension practice demands a surplus distribution, I naively thought a second advocacy request to CARP would be as successful as the first. Moses Znaimer, president of CARP, sat beside me and thanked me for the information. I naively thought that CARP would investigate and then advocate, putting CPP reform next on Finance Minister Morneau’s legislation list. Democracy demands CPP reform because roughly 99% of Canadians would benefit immensely from it, as shown below.

How wrong I was. For eight years, despite repeated pleas from me, CARP never even acknowledged the surplus. Why would one justifiable issue to help seniors receive instant action from CARP and Mr. Morneau and the other receive a brick wall? CPP reform would result in our financial industry eventually losing billions of dollars, per year and actuaries experiencing a huge drop in employment. Below explains in detail.

The losses for the financial industry could be astronomical

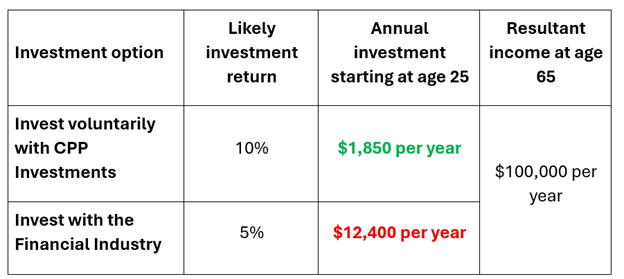

As shown at www.fixthecpp.ca, it is likely a 25-year-old will have a $100,000 CPP pension in 2026 dollars, making any investment for retirement somewhat unnecessary. And for those who want to invest, probably 99% of Canadians would recommend permitting voluntary contributions to CPP Investments. The table below shows why.

These facts show that the financial industry could lose billions of dollars in investment fee profit, per year, if this news were publicized. Regrettably, as shown, here, the above information has never reached Canadians, most who are struggling financially.

The financial industry is aware and concerned

In 2016, the CPP’s surplus was roughly $100 billion. When Finance Minister Bill Morneau announced lacklustre, more-of-the-same CPP changes, Janet Ecker, President of the Toronto Financial Services Alliance, expressed relief. Even ten years ago, when the CPP’s surplus and potential were not substantial, she feared significant CPP reforms like voluntary contributions could:

"Undermine a lot of successful, legitimate, (retirement savings) products in the investment industry."

But who should be “undermined”?

Should it be an industry packed with millionaires that already captures 47% of all Canadian corporate profits?

Or should it be the millions of Canadians struggling near insolvency? The 99% are now needlessly investing towards retirement, achieving the low returns that the financial industry can give them?

The financial industry should share more profit with non-financial industries

Some economists would suggest, “If a company earns x% of corporate profit, in an ideal world, they should contribute x% to our GDP.” With the financial industry earning 47% of all corporate profit but only contributing 7.4% to our GDP, a reduction in their profit is arguably appropriate.

Moreover, while the financial industry may lose profit share with the recommended legislation, other industries will gain profit share. Canadians will have as much as 15% more income to spend today instead of investing for tomorrow. This means that, for Canada’s non-financial industries, sales, productivity and profit will increase, along with Canada’s anemic GDP.

Does the financial industry have enough resources to engineer a cover-up?

Our financial industry has both the economic justification and the resources to orchestrate this widespread cover-up. Just 1% of their annual profit is $1.6 billion, equivalent to 160 convincing “packets” of $10 million each. Consider it a business expense with a high return on investment. For example, a $1.6 billion expenditure per year today might result in an ongoing $5 billion profit flow per year for years to come.

How did the financial industry orchestrate such a devastating cover-up

Firstly, because the news of the CPP’s surplus and potential would lead to a reduction in other pension funds (and the actuaries who oversee them) and a reduction in the need for life insurance, the evidence indicates the entire actuarial profession has joined the cover-up as shown here.

Then, probably using their deep pockets, the financial industry needed to convince the media to never mention the CPP’s surplus as shown here. And when Premier Smith would not cooperate, they persuaded the actuarial profession and media industry to combine forces to portray Premier Smith as unhinged. However, because Premier Smith has notified Albertans they will receive as much as $10,000 each when Alberta receives its fair share of the CPP fund, there is a growing movement in Alberta towards separation from Canada.

As described earlier, the benefits available to 99% of Canadians far outweigh the drawbacks the financial industry would experience. How did the financial industry convince politicians to remain silent on such a crucial topic?

Lobbyists have tremendous influence

Lobbyists are unethical, educated, knowledgeable, persuasive economists, actuaries and policy experts who are well paid to use devious means to convince politicians that certain legislation would benefit all Canadians, not just their employer. They usually represent an industry or company. Busy politicians have little time to investigate all issues so they rely on lobbyists to “educate” them.

Recent data shows lobbyists had 31,058 recorded lobbying meetings in one year with federal officials. The financial industry is the most active lobbying industry in Canada. They are eager to maintain their 47% share of all corporate profit. The evidence leads one to believe they have used fallacious but convincing arguments regarding suppressing the news of the CPP’s surplus and potential. They probably presented an argument that indicates giving Canadians the considerable benefits available from CPP reform would somehow lead to “economic Armageddon.” They also may have used some of their billions of profit dollars to “influence” politicians through campaign donations, no-interest loans or bribes.

Politicians “drank the Kool-Aid” and defied all principles of democracy. All MPs now refuse to even acknowledge the CPP’s $500 billion surplus, even though it could lead to considerable improvements in the lives of 99% of Canadians, and bring roughly $10,000 to each of their constituents.

Conversely, individual citizens, poverty activists or citizen groups rarely meet with ministers. When I met three of my four MPs, they all agreed to pass my findings on the CPP’s surplus to their party’s Finance critic. Nothing more happened.

My fourth MP, the principled Jane Philpott, was ejected from the Liberal Party because she acted too ethically. She disobeyed Prime Minister’s demand to ignore rampant corruption when SNC-Lavalin paid tens of millions in bribes to Libyan officials in order to win lucrative contracts. Not only did Prime Minister Trudeau sanction the bribes, he expelled any MPs who wanted greater transparency regarding the issue.

Would Prime Minister Carney, a veteran of the financial industry, similarly expel MPs who spoke out regarding the CPP’s surplus?

After receiving a presentation regarding the CPP’s surplus, Ms. Philpott’s final words to me were “Disgraceful lobbyists.”

Our financial industry has already achieved considerable benefits from our politicians. Lobbyists are probably responsible for the creation of programs such as RRSPs and TFSAs. They both provide significant, fully legal tax advantages to Canadians who invest through the financial industry who invest $138 billion per year using them as their investment vehicle. Governments have also introduced a range of other policies and incentives that consistently encourage investment by Canadians, eager to avoid a retirement in poverty..

The result is clear: Canadians have directed trillions of dollars into these vehicles, generating an estimated $30 billion annually in fees and revenues for the financial sector.

Yet many Canadians are unaware of the extent of public support already built into the system. For example, a single senior with no income can receive approximately $22,000–$23,000 per year through Old Age Security (OAS) and the Guaranteed Income Supplement (GIS). In addition, up to $5,000 from employment is not subject to any tax or clawback. Finally, withdrawals from a TFSA remain fully tax-free.

Despite this considerable security Canada guarantees low-income seniors, the prevailing message from the financial industry is broadcast repeatedly—“Save aggressively now or face a retirement in poverty.” In reality, the system already provides a meaningful income floor, which significantly alters the level of private saving required today.

Think tanks only advocate for the wealthy

Ten years ago, I naively thought think tanks were the ultimate authority, packed with scholars who analyzed complex issues and arrived at the best solution for all Canadians and Canada. Then, upon seeing their analysis of the CPP, packed with misinformation and deception, I researched who funds Canadian think tanks.

On Think Tanks (OTT) is an international organization dedicated to exposing how transparent think tanks are worldwide. Astonishingly, they report that Canada is even less transparent than the US and the UK. Below is a report showing how much each Canadian think tank reveals who funds them.

The think tank that reveals the sources of all funding receives a five-star rating. The think tank that reveals nothing about who funds them receives a zero-star rating. The more transparent organizations in the top half of the table predominantly focus on non-financial issues.

All of the organizations in the bottom half of the table have received these details regarding the CPP’s surplus and potential. None have responded or acted, thereby contradicting their admirable mandate. It is likely that the hidden funding for think tanks with few stars is from the financial industry.

Malcolm Hamilton, the senior actuary who failed in his 40-hour attempt to suppress my findings, is associated with the C.D. Howe Institute. In 2020, C.D. Howe published a misleading report that claimed there is giant risk associated with the CPP, when it had a $300 billion surplus. The C.D. Howe Institute hosts 90 meetings a year that are mysteriously “off-the-record”. Was an elaborate bribery campaign planned in these meetings? We will never know.

Regrettably, politicians use think tanks extensively to formulate government policy. Globe and Mail reporter Konrad Yakabuski explains.

“Between 2000 and 2015, representatives from Canada's 10 leading think tanks appeared at least 216 times before parliamentary committees and were cited in the Canadian media almost 60,000 times. It gave them and their research priceless exposure and influence in shaping government policy.

But at what price to Canadian democracy?

There is little doubt that the research conducted by Canadian think tanks often enriches public-policy debates. While they claim to be independent, however, most think tanks rely on funding from wealthy benefactors, corporations, unions or lobby groups seeking to push their own causes.

In April 2017, the average transparency score among the top 10 was a miserable 1.5 stars.”

How the financial industry is trying to keep investors investing with them

With legislative changes:

25-year-old Canadians could reasonably expect a CPP pension of $100,000 in 2026 dollars,

Canadians could be allowed to invest $1,000 per year, for example, with CPP Investments, generating as much as three times the profit when compared to investing with the financial industry.

Knowing this, young Canadians would stop investing with the financial industry, stop investing in other pension funds and stop buying life insurance.

CPP Investments’ mandate now lets them invest worldwide, seeking the best return with minimal risk. However, in May 2026, our media, controlled by the financial industry, focused on demanding legislation that forces CPP Investments to invest more in Canada, even if the investments are not as profitable. Most Canadians, unaware of the CPP’s surplus and potential, probably agree with this idea that would create jobs and stimulate our economy.

However, if such legislation were passed, Canadians would lose billions and the financial industry would gain billions because:

CPP Investments, somewhat handcuffed, would generate lower returns,

the above benefits would then be less likely,

Canadians would more likely continue to invest with the financial industry, buy life insurance and contribute to other pension funds.

the financial industry and actuarial profession would continue to collect billions in profit that they do not deserve.

For perspective, if you self-invest, how would you like it, and how much lower would your returns be, if the entire Canadian investment community told you that you can only invest in Canada.

Numerous otherwise benevolent organizations needed to be silenced

The influence of the financial industry must be enormous. I have sent these details to numerous organizations, all with benevolent mandates. They all failed to respond or advocate. They are acting as if the financial industry has accompanied a generous “donation” with a message like the following:

“Please meet your mandate and advocate strongly against any injustice you find. However, never mention the CPP’s surplus. If you do, your annual donation will stop.”

When these otherwise reputable organizations never mention any existence of a cover-up, Canadians understandably conclude that there must not be a cover-up. These organizations not only fail to advocate. They lull Canadians into assuming no cover-up is possible.

Executives in these reputable organizations may have decided this alleged donation/bribe will considerably help them accomplish their organization’s goals in all areas except one. Or the donation/bribe may have mostly ended up in the executive’s personal bank account.

There is nothing illegal regarding this unwritten agreement. It is not a bribe, they can argue. It is merely donation with an understanding. In the event of an investigation, participants have little to fear. However, our CRA does frown on non-profits and charitable organizations that publish a mandate, collect membership fees based on that mandate and then ignore their mandate. For example, CARP is Canada’s most powerful advocate for seniors, especially on financial issues. Seniors conservatively deserve $60 billion from the CPP’s surplus. Yet CARP remains silent.

If you have doubts about these accusations, you may want to contact an organization of your choice, alluding to this website’s findings and asking them why they are not advocating aggressively for CPP reform.

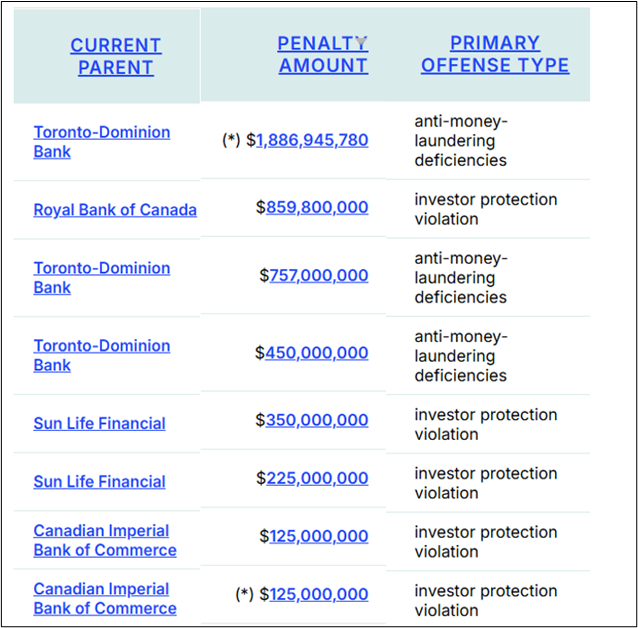

Are banks, the lion’s share of the financial industry, without sin?

Banks in Canada give their customers a sense of professionalism, helpfulness and integrity. Most customers probably leave thinking “Those nice people at my bank would never abuse me.” Yet Canada’s banks have been found guilty of numerous violations, mostly related to not protecting investors.

Violation tracker is a worldwide database summarizing corporate misconduct. Below is a screen capture of a report showing the members of Canada’s financial industry that have been found guilty of financial crimes, with the size of the fine shown to the right.

The screen shot above lists the largest of 106 violations. For every financial crime committed, estimates vary regarding how many other violations never result in prosecution. Some say the ratio is 1 to 5. Others say 1 to 50. That means that, for each violation listed, there are another 5 to 50 violations taking place that are not being prosecuted. And how many more go undetected by the prosecutors, hampered by a minimal budget.

Big bank presidents, who all earn $10-$20 million per year, work hard to satisfy shareholders with higher profits. If secretly abusing customers with no consequences, or periodic fines, will increase profit, bank presidents will sanction such abuse.

With billions of profit dollars at stake if the news of the CPP’s surplus is revealed, it is reasonable to suspect Canada’s financial industry engineered a media blackout and somehow silenced all politicians, except Premier Smith, regarding the CPP’s $500 billion surplus.

If there is no cover-up, why did Premier Smith promise Albertans big benefits

The above allegations may be difficult for Canadians to believe - deceptive actuaries, a muzzled media, organizations ignoring their mandate, and politicians inert. However, the Charbonneau Commission uncovered a cover-up of similar scale as shown here.

Roughly three years ago, all Premiers and their Finance Ministers received these details claiming 20 million CPP members deserve $10,000 each from the CPP’s surplus. One agreed and acted.

Premier Smith may be the most honest politician in Canada, refusing to let Toronto’s Bay Street millionaires profit while Albertans suffer. She has demanded Alberta’s share of the fund and, when she receives it, she has promised to give all Albertans as much as $10,000 each. Albertans may soon vote to separate from Canada if Ottawa does not cooperate regarding the CPP, as shown here.

Should a few thousand financial executive earn millions while the 99% struggle

Three associates from university joined the financial industry and now worth an estimated $100 million each. In December 2025, Canada’s big banks distributed $27.3 billion in bonuses. How many benefitted? One estimate suggests 15,000 bank employees received $1.8 million each, on top of their salaries.

The financial industry has rigged our capitalist system so that they can continue to earn billions of dollars by depriving 99% of Canadians, most struggling, of hundreds of billions in deserved benefits.