Why and how actuaries have betrayed all Canadians

Actuaries have both the motivation and the opportunity to conceal the CPP’s $500 billion surplus.

The motivation

Roughly nine years ago, I queried several top actuaries on why they were not announcing to Canadians the wonderful news:

“Our CPP fund now has a huge surplus and, based on standard pension practice, every member of the CPP will be receiving a $10,000 payment, on average, from that surplus. And there will be no risk to future CPP pensions.”

Most of the CPP’s 22 million members have invested 10-12% of their lifetime earnings with the CPP. Given the complexity of pension mathematics, Canadians must rely heavily on actuaries—among the most highly trained quantitative professionals—to assess and safeguard these contributions.

At first, I assumed any discrepancy was simply an oversight. Governments make errors; perhaps this was one. I expected that once identified, it would be acknowledged and addressed.

Instead, when I raised the issue with ten experienced actuaries, the responses were consistently dismissive or highly technical, without directly engaging the underlying question. They probably hoped their stranglehold on actuarial mathematics would make any would-be investigators like me disappear.

However, over the last ten years, one statement has echoed in my mind unanswered.

“How could I receive $20,000 from the Ryerson University Pension Plan’s 18% surplus and Canadians not receive a surplus payment when the CPP had, at the time, a 100% surplus?”

The CRA ordered the distribution of Ryerson’s surplus. Why was our Chief Actuary not following the CRA’s policy, which would bring huge relief to millions of struggling Canadians.

It took me several years to understand why all actuaries as a profession have uniformly adopted a stance matching that of our Chief Actuary who has stated to me,

“The CPP is not in surplus. No further comment.”

Here is why. Because CPP investment will likely continue investing so successfully, young Canadians can anticipate a likely $100,000 CPP pension in 2026 dollars. If young Canadians learn a $100,000 CPP pension is likely, they will refuse to contribute to other pension funds. Many pension funds would then gradually become extinct, and so would lucrative employment for the actuaries that must oversee them. The CPP could eventually become Canada’s only pension fund, providing Canadians with a much bigger pension based on a much smaller total contribution to just the CPP.

Also, consider life insurance. The CPP now provides surviving spouses with as much as 60% of their partner’s pension, which eventually could be as much as $60,000 per year, indexed to inflation. Why buy life insurance when the CPP already provides the equivalent benefit at no extra charge? To receive an indexed $60,000 per year life insurance benefit, a Canadian might need to pay $1 million in premiums.

Roughly 50% of employment for actuaries is in the pension fund and life insurance business. If the CPP’s surplus and potential becomes known, employment for actuaries will decline considerably.

It was difficult for me to believe a profession trusted to safeguard 10-12% of most Canadians’ lifetime earnings would stoop so low to protect their ongoing employment prospects. However, their actions, the motivation, and the overwhelming evidence indicate they have.

The opportunity

For most Canadians, if their bank intentionally tried to shortchange them of, for example, $100, they would likely detect it and aggresively demand an apology. However, they are in the dark on how their CPP contributions are being handled.

This is because actuarial science is highly complex. Every three years, our Chief Actuary produces a report roughly 200 pages long that is packed with complex daunting mathematics that almost all Canadians would never want to assess.

Meanwhile, if you include employer matching on our behalf, all Canadians contribute 10-20% of their income to pension funds, all monitored exclusively by actuaries. Canadians are forced to trust these actuaries to treat their considerable pension contributions with appropriate care and justice, using advanced actuarial mathematics.

Simplifying the actuarial analysis of our CPP contributions

How can a professor who taught The Mathematics of Finance challenge the findings of our Chief Actuary when actuaries are “experts” in pension fund analysis. Roughly 90% of our Chief Actuary’s analysis involves actuarial mathematics and is reasonably accurate. However, the financial component of our Chief Actuary’s analysis is highly flawed and should arouse deep suspicion among Canadians. This is because exposing the truth could lead to employment for actuaries cut in half.

While our Chief Actuary has produced thousands of complex pages for the public to view regarding the status of the CPP, there are only two factors that impact a surplus or deficit in a pension plan - Net Cash Flow and Investment Return.

Net Cash Flow is the amount remaining after contributions from working Canadians are reduced by pension payments to retirees. When estimating this figure for the next 75 years, actuaries use complex mathematics to analyze long-term demographic and economic factors including inflation, immigration, fertility rates, employment levels and mortality rates. (On September 11, 2024, Finance Minister Freeland emailed me why the CPP is not declaring a surplus. She claimed we need the surplus because baby boomers are retiring. Actuaries have already 100% accounted for the influx of baby boomers as pensioners and their longevity in their analysis.)

Approximately 90% of actuarial reports on the CPP deal with estimating Net Cash Flow.

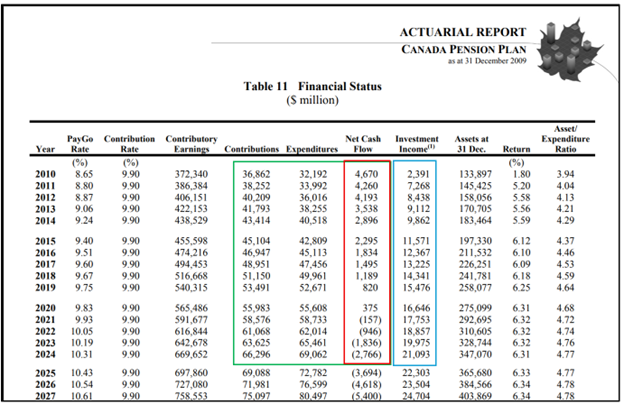

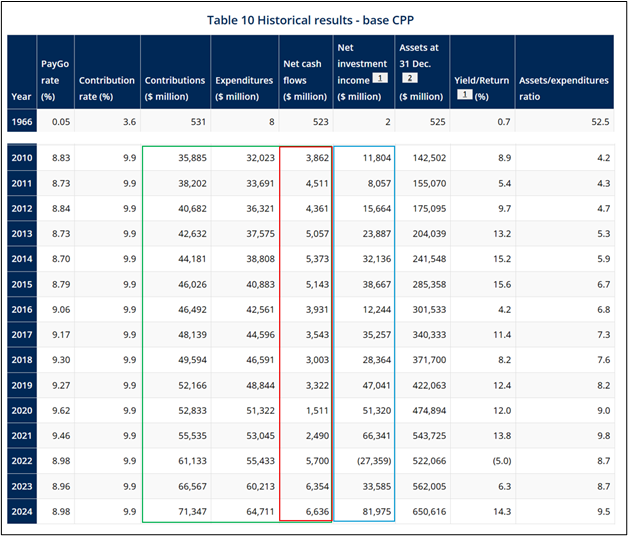

Over the past fifteen years, our Chief Actuary has been remarkably accurate estimating Net Cash Flow. The red box below shows the predictions he made in 2010 for Net Cash Flow from 2010 to 2024. The total of the red box below is $22 billion.

The actual values for Net Cash Flow, from the 32nd Actuarial Report, published in 2025, show he has underestimated Net Cash Flow. The total of the red box below is $65 billion.

Summarizing, on all aspects of actuarial science except investment return, in 2010, our Chief Actuary estimated the fund would have a $22 billion positive Net Cash Flow from 2010 to 2024. The actual positive cash flow was $65 billion, $43 billion above the estimate. This $43 billion has contributed roughly 8.6% to the CPP’s $500 billion surplus today and reinforces the argument justifying a CPP surplus distribution now.

Investment Return is the other factor that impacts on a pension fund’s funded status. It does not require advanced actuarial mathematics. Since 2010, our Chief Actuary has stated, “Our CPP fund will be 100% funded if Investment Return is roughly 6% per year.”, as shown in the second column from the right in the 25th Report. Meanwhile, CPP Investments has averaged a 10% return per year since 2010, as shown in the second column from the right in the 32nd Report.

The difference is astounding. If, for example, you invested $10,000 with a 6% return for 15 years, you would have $24,000. With a 10% return, you would have almost twice as much, $42,000.

The blue columns in the two reports, Investment Income, show the impact of a 6% return versus a 10% return. In the 25th Actuarial Report, the blue box shows our Chief Actuary predicted investment income totalling $199 billion. In the 32nd Actuarial report, the blue box shows the actual investment return, totalling $459, resulting in an indisputable $260 billion surplus. In 2025, the surplus increased by an additional $53 billion, resulting in a $313 billion surplus.

However, because CPP Investments has averaged a 10% return for 15 years, and has many advantages over the average investor, an ongoing 10% return is likely. Pension fund experts insist on using the most accurate prediction of investment return or generational equity principles are not addressed. Specifically, pensioners will die never receiving their fair share of the surplus, which was accumulated investing their money. Presuming an ongoing 10% return, the required fund size to fund all promised pensions becomes considerably smaller and the surplus becomes considerably larger. That is why, in 2026, our $781 billion CPP fund is $500 billion above what is needed to fund all CPP pensions for the next 75 years.

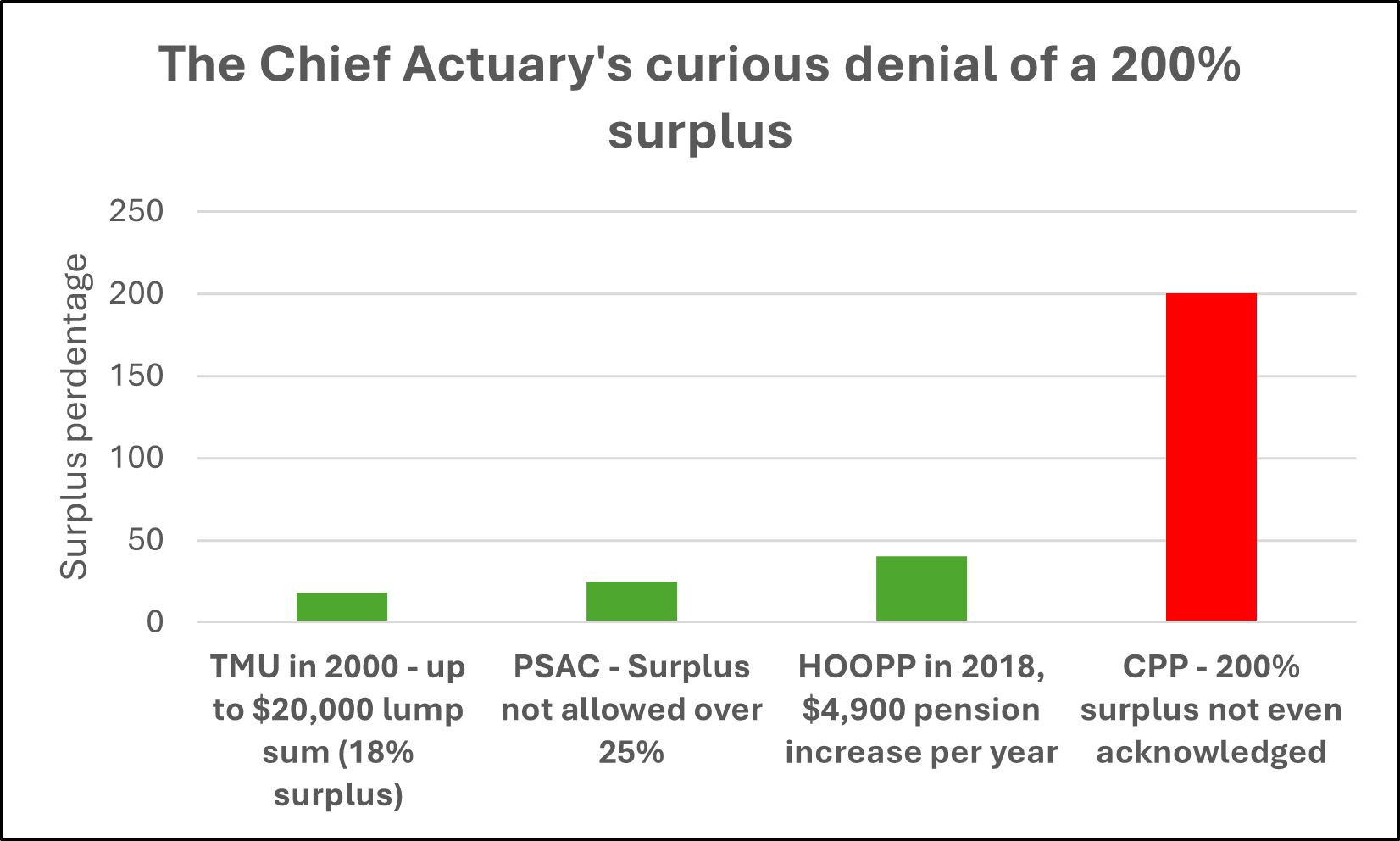

Other pension plans act when the surplus is over 25%

In 2000, the Ryerson University (now TMU) Pension Plan had an 18% surplus. Professors, including your author, received as much as $20,000 each. The CRA ordered it.

Preceding 2018, the HealthCare of Ontario Pension Plan (HOOPP) had a substantial surplus because of shrewd investing. The HOOPP Board of Governors, composed primarily of contributors and pensioners, declared a surplus payment that increased all pensions by roughly $4,900 per year.

The Public Service Alliance of Canada (PSAC) represents approximately 245,000 members, including federal public service employees, university staff, and other public sector workers.

Our Chief Actuary, who also oversees the PSAC pension plan, has stated,

“Federal rules say the plan cannot hold a surplus of more than 125% of liabilities, defining such amounts as a ‘non-permitted surplus’”.

Why would our Chief Actuary never acknowledge the CPP’s 200% surplus, 300% of liabilities, but announce the PSAC’s 25% surplus as a “non-permitted surplus”?

Comparing pension plan surplus amounts and actions by overseers

When our Chief Actuary was asked to comment, he responded via email that “The CPP is not in surplus” and “No further comment”. Despite irrefutable evidence the CPP now has a $500 billion surplus, he has never mentioned “surplus” in his thousands of pages of reports produced since 2010.

One of Canada’s top actuaries is Malcolm Hamilton. In 2020, he contacted me and we debated the existence of the surplus, first, in person and then via email for roughly 40 hours. He tried to silence me with vacuous arguments. It is possible he was hired by the actuarial profession to convince me to silence my claims?

Since our meeting, the CPP’s surplus has increased by another $300 billion.

One of the actuaries I consulted did have a conscience. He stated,

“Our Chief Actuary has done what pension actuaries frequently do - invent measures that are easily manipulated so that actuaries can control the narrative and hide things at will...I must remain anonymous because I am not allowed to criticize my fellow actuaries.”

As someone who has studied thousands of pages produced by our Chief Actuary, I heartily concur with this disappointing assessment of the individual who Canadians trust to safeguard our trillions of dollars in CPP contributions.

How does the Chief Actuary justify a system in which the Canada Pension Plan is not subject to oversight by the Auditor General, the Canada Revenue Agency, or a representative board of contributors and beneficiaries?

His position is that an external peer review by his fellow actuaries ensures the accuracy of his work. However, concerns arise when a member of the profession has stated, “I am not allowed to criticize my fellow actuaries”. In that context, the effectiveness of such reviews may reasonably be questioned, as they risk functioning more as rubber stamp than as independent scrutiny.

After 2010, when the fund was 100% balanced with no surplus, this inconvenient surplus started to mushroom. Actuarial reports after 2010 were packed with deception and misleading reporting. Our Chief Actuary has “cooked the books” to hide the surplus. For example, even though CPP Investments has averaged a 10% return for 15 years, our Chief Actuary bases all his calculations on a 6% return for the next 75 years.

An accurate forecast of investment returns is crucial. Respected pension expert, Jim Keohane, oversaw the Healthcare of Ontario Pension Plan (HOOPP) for many years. HOOPP has had investment success similar to CPP Investments. However, unlike the CPP, HOOPP’s Board of Governors includes many contributors and pensioners. Because the HOOPP fund had accumulated a large surplus, the HOOPP Board of Governors increased all pensions by $4,900 per year on Jan. 1 , 2018.

Mr. Keohane has stated

“If you use any discount rate [forecasted return] other than the best estimate of future returns on the portfolio you are going to overfund or underfund the obligation which brings up a whole series of intergenerational fairness issues”.

But what does “intergenerational fairness” actually mean in practice?

Since 2016, roughly one million low-income seniors have died without ever receiving what could have been a surplus payment of approximately $10,000 each—a sum that could have increased their modest incomes by as much as 40%. Another 100,000 financially struggling seniors will die this year without seeing any such benefit.

Speaking personally, as a 78-year-old, I know how much income matters. Without my professor’s pension, my quality of life would not decline marginally—it would collapse.

And what of younger Canadians?

What of the 43% of Canadians who are within $200 of insolvency? What of a system that does not distribute a 200% surplus, when standard pension practice would trigger a distribution at when the surplus is just 25%?

If “intergenerational fairness” means anything, it must apply to those living today—not just to theoretical future cohorts.

Instead, Canadians are left with a system in which trillions of our hard-earned dollars are managed with suspect, self-serving oversight, while millions struggle financially.

A fox is guarding a henhouse that holds 10-12% of most Canadians’ lifetime earnings. The question is unavoidable: whose interests are truly being protected?

Any evasive argument by actuaries can be dismissed with proof

The CPP is a pay-as-you-go pension plan - some contributions from younger Canadians are used to pay pensions for older Canadians. This policy is risky for private sector plans because, when a firm goes bankrupt, the fund will not have enough to pay all promised pensions. However, Canada will never go bankrupt. There will always be employed Canadians who must contribute as much as 6% of their income, matched by their employer, to the CPP. Our Chief Actuary, in his calculations regarding the status of the CPP, has fully accounted for this pay-as-you-go aspect of the CPP.

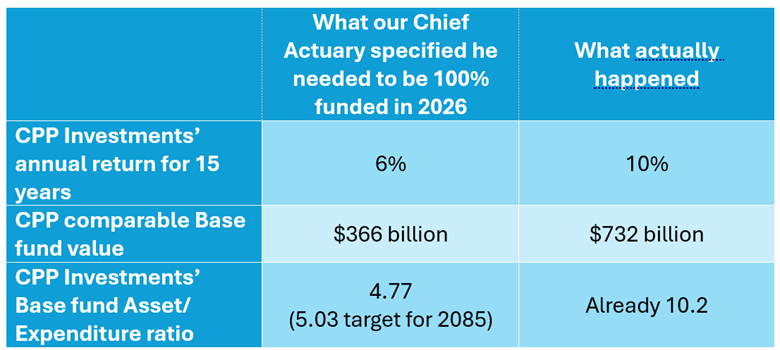

Our Chief Actuary may claim he is letting the surplus grow to move from pay-as-you-go financing to steady-state financing. The following is from Page 69 of his 25th Actuarial Report.

“The reform package agreed to by the federal and provincial governments in 1997 thus included significant changes to the Plan’s financing provisions: The introduction of steady-state funding to replace pay-as-you-go financing in order to build a reserve of assets and stabilize the ratio of assets to expenditures over time.

Under steady-state funding, the ratio of assets to expenditure is currently projected to stabilize at a level of about 4.7. (It is now 10.2) Investment income on this pool of assets is projected to help pay benefits when the large cohort of baby boomers retires. This refers to section 113.1(4)(c) of the Canada Pension Plan.”

Even though the Asset/Expenditure ration is more than double what is required for stability, our self-serving Chief Actuary will invoke confusing terms like sustainability, minimum contribution rate, steady-state financing, pay-as-you-go, and more to defend his failure to jubilantly tell Canadians our CPP fund has a huge surplus because of outstanding investment returns. The table below shows why all of these confusing terms cannot overcome the truth.

Comparing predictions to reality

The Asset/Expenditure ratio divides the value of the fund on Dec. 31 by the forecast of pension payments for the following year. The larger the ratio, the bigger the surplus. Because 9.8 is more than double 4.77, we could distribute half of the $705 billion base fund and still meet the Asset/Expenditure target.

No matter what confusion our deceptive Chief Actuary presents, he cannot avoid the facts in the table above.

In addition to the complexity of actuarial mathematics, our Chief Actuary has taken advantage of the fact he is not audited. Our Auditor General frequently reviews public sector pension plans like those for members of the RCMP, National Defence and PSAC. His review contains these logical, encouraging words.

“According to best practices, properly designed governance should focus on implementing the principles of fairness, accountability, and responsibility to all stakeholders.”

With the CPP, neither our Auditor-General nor our CRA has any jurisdiction.

Moreover, pension experts recommend every pension fund has a Board of Governors, primarily made up of contributors and pensioners. The CPP has no such Board. Our Chief Actuary has full control. Yet he has never mentioned “surplus” in thousands of pages of reports on the status of the CPP. To protect his at-risk industry, instead of notifying all Canadians of wonderful news, he has buried a $500 billion surplus.

Keith Ambaschtsheer is Director Emeritus of the International Centre for Pension Management (ICPM). He devoted 82 pages to “Pension Governance” in his recently published book The Future of Pension Management. The 82 pages virtually demand that every pension fund have a Board of Governors, mostly comprised of contributors and pensioners. Page 70 states

“Board members must be collegial, representative and make a collective commitment to understand and fairly balance stakeholder interests.”

Mr. Ambaschtsheer would be ideal as a member of a CPP Board of Governors, joining representative contributors and pensioners like you and me. When asked if he was interested in being a member, he refused, saying “I am just a humble financial economist”. It should be very disturbing to Canadians when a top pension expert, who has written 82 pages on the need for a Board of Governors, refuses to become a member of a CPP Board of Governors, citing inadequate qualifications. If the CPP did create a representative board, other pension funds, which are his source of income, would become less necessary.

Conversely, CPP Investments has an excellent board. However, their board only oversees investment decisions, not surplus distribution issues. Perhaps because these board members all come from the financial industry, they remain mysteriously mute regarding the CPP’s $500 billion surplus and potential to solve the serious financial problems facing many Canadians today.

One million seniors have died earlier than they should

Generational equity, or fairness to all, is rightfully the goal of all pension fund managers. Younger members of a pension fund should be treated with the same justice that older members are. If CPP Investments used our money to create the $500 billion surplus, young and old Canadians should each receive their fair share, leaving a 25% surplus. If generational equity is not addressed, older Canadians will die, never receiving their deserved surplus payment.

Since 2016, approximately one million low-income Canadian seniors have died. Two thirds were women. If our Chief Actuary had followed standard pension practice, these older Canadians, trying to exist on an income of roughly $25,000 each, would have received approximately $10,000 each.

Numerous studies show higher income leads to a longer life. One study found that people in the highest income quintile live 13 years longer than those in the bottom quintile. A $10,000 surplus payment for these struggling seniors could have led to a longer life for them.

And their quality of life in the final years would have improved. With this 40% raise in income, many, instead of existing indoors, would have been able to, for example, dine out, travel, play sports, meet socially, take uber, meet a partner, and more.

Because politicians and our Chief Actuary refused to follow standard pension practice, and stood idly by as our media vetoed this story, many of these one million low-income seniors died earlier than they should, with a lower quality of life.

Consider a scammer who managed to acquire a struggling senior’s bank password and drained his last $10,000 from his bank account. Canadians would be outraged and demand considerable jail time for the scammer. What is the difference between what that scammer accomplished and what the actuarial profession has accomplished by keeping a deserved $10,000 out of the bank accounts of two million low-income, struggling seniors? The only difference—the actuarial profession’s impact is two million times the impact of the scammer. And that comparison only considers low-income seniors, not the 43% of Canadians who are within $200 of insolvency.

If our Chief Actuary claims there is no CPP surplus when there is an irrefutable $500 CPP billion surplus, he needs to explain to Canadians why he is not following generational equity concepts and standard pension practice. The impact of his silence on such a crucial topic is huge. While it is unsavory, on behalf of millions of struggling Canadians, it needs to be stated. When one intentionally shortens the lives of a large number of people, it is called genocide.

Actuarial deception may lead to Alberta leaving Canada

A major reason that Albertans are considering separation is because actuaries and Ottawa refuse to distribute a Canada-wide CPP surplus payment. Moreover, the actuarial profession has joined the media in spreading false information about the only senior Canadian politician willing to combat this insidious cover-up, Premier Danielle Smith. The full story is here.

Access to Information gives curious Canadians zero

Even though:

Our CPP fund holds 10% of the lifetime earnings of most Canadians on their behalf,

Our Chief Actuary, in a conflict-of-interest position, is audited by no one,

Our media refuses to even mention the CPP’s irrefutable $500 billion surplus,

All MPs remain silent when standard pension practice would give their riding’s citizens $10,000 each, $76 million,

my request for information was 95% redacted. The request related to:

Tasking the Chief Actuary on Asset Transfer if Alberta exits Canada Pension Plan (CPP)

The only text in the five-page document received was quotes from the Canada Pension Plan Act. The rest of the document was entirely redacted.

An accurate forecast of investment returns is crucial. Respected pension expert, Jim Keohane, oversaw the Healthcare of Ontario Pension Plan (HOOPP) for many years. HOOPP has had investment success similar to CPP Investments. However, unlike the CPP, HOOPP’s Board of Governors includes many contributors and pensioners. Because the HOOPP fund had accumulated a large surplus, the HOOPP Board of Governors increased all pensions by $4,900 per year on Jan. 1 , 2018.

Mr. Keohane has stated

“If you use any discount rate [forecasted return] other than the best estimate of future returns on the portfolio you are going to overfund or underfund the obligation which brings up a whole series of intergenerational fairness issues”.

Our Auditor General frequently reviews public sector pension plans like those for members of the RCMP and National Defence. His review contains these logical, encouraging words.

“According to best practices, properly designed governance should focus on implementing the principles of fairness, accountability, and responsibility to all stakeholders.”

Recall, for example, the sponsorship scandal.

“The scandal involved the misappropriation of millions of dollars of taxpayers’ money that had been illegally channeled into the pockets of advertising executives and others close to the Quebec wing of the Liberal Party.”

Who was crucial in determining the guilt of the Liberal Party?

“In early 2004, Auditor General Sheila Fraser delivered a damning report, finding that approximately $100 million, in the form of fees and commissions, had been paid to advertising and communications companies operating in Quebec, often for work that was not even done.”

It was the work of our Auditor General that revealed this $100 million scandal to Canadians. The size of the CPP scandal is $170 billion, 1,700 times as much. And, unlike the sponsorship scandal, it is money coming directly out of our pockets, not the general government account.

Ontario’s Auditor-General, Bonnie Lysyk, should audit the CPP because she does not answer to politicians. In her December 2021 report, she bravely accused Premier Ford of vetoing legislation that would benefit the smaller investor while reducing the profits of the investment industry. She stated that “intense lobbying” has been “a significant contributing factor”, resulting in smaller investors losing $13.7 billion since 2016.

Ms. Lysyk’s report confirms three things related to the CPP:

The financial industry uses “intense lobbying” to sway politicians to legislate in their favour. In this case, lobbying has cost the smaller investor $13.7 billion while increasing the profit of the financial industry by $13.7 billion. It is likely that, with $13.7 billion at stake, the lobbyists made secret large donations to the Conservative Party and/or Mr. Ford.

Politicians can be swayed by lobbyists to ignore smaller investors, even though they will lose thousands of votes.

Mr. Ford, who constantly alludes to protecting “the little guy”, is a hypocrite.

If Ms. Lysyk audited the CPP, you would probably be soon receiving a deserved CPP surplus payments.

What did Ms. Lysyk mean by “intense lobbying”? Did the lobbyist yell at Mr. Ford? Did he spill coffee on him? Or did he simply say,

“The consequence of not listening to us will be a withdrawal of our legal and secret donations to your political party and you.”

Such a statement explains Mr. Ford’s behaviour. And the amount of the donation may be substantial with $13.7 billion at stake. He may have said to himself

“Because I am abusing smaller investors, I will lose some votes. However, I need to keep that gravy train of secret and legal donations going, so why not abuse a few smaller investors.”

The CPP and our deceptive Chief Actuary need to be audited by a fearless auditor like Ms. Lysyk, who solely represents the interests of Canadians and is willing to reveal how lobbying is depriving millions of “little guys” of billions of deserved dollars.

An unsuccessful attempt from a top pension expert

Because I emailed several politicians about the CPP’s surplus, top pension expert Malcolm Hamilton contacted me in 2019. We met for four hours in person and then exchanged lengthy emails that resulted in roughly 40 hours of time spent by each of us.

Using vacuous arguments, Mr. Hamilton attempted to convince me that the CPP does not have a surplus. It is difficult to convince a Professor of Finance that 2+2=5. It is difficult to claim there is no surplus when there is an irrefutable $257 surplus. Mr. Hamilton could not provide any viable reasons to NOT distribute $170 billion of the CPP’s surplus.

Why would a top Canadian actuary spend 40 hours trying to convince me that there is no surplus? Was it to protect his at-risk industry that could be decimated because the CPP could evolve into the only pension fund needed in Canada?

The C.D. Howe Institute is a think tank that refuses to reveal who funds them, according Transparency International. The institute recently published a disgraceful misinformation paper with the heading “Uncertainties loom for the Canada Pension Plan”, claiming our CPP pensions may be in jeopardy. It is packed with deception and mistruths. Mr. Hamilton has worked for the C.D. Howe Institute.

Is this who you want monitoring 10% of your lifetime earnings?

One top actuary I contacted, likely in a moment of conscience, stated the truth. He said our Chief Actuary

“has done what pension actuaries frequently do - invent measures that are easily manipulated so that actuaries can control the narrative and hide things at will.

I must remain anonymous because actuaries are not supposed to criticize other actuaries.”

As someone who has studied the CPP for over five years, I heartily concur with this disappointing assessment of our Chief Actuary.

Twenty million Canadians have as much as 10% of their lifetime earnings monitored by a Chief Actuary who:

“invents measures, manipulates data, controls the narrative, and hides things at will”,

denies an irrefutable $257 billion surplus,

forecasts using a 5.5 % return for CPP Investments when they have averaged 11% for nine years, thereby burying the surplus,

does not report to a representative Board of Trustees,

is not audited,

is only peer-reviewed by actuaries who “are not allowed to publicly criticize other actuaries”,

is depriving 17 million Canadians of a deserved $170 billion,

is depriving our sputtering economy of a needed $170 billion stimulation,

is depriving our deficit of a $50 billion reduction,

is preventing a logical solution to mushrooming income inequality.

To summarize, an actuarial fox is guarding our CPP henhouse, which holds trillions of our hard-earned dollars. There are zero checks and balances.

For these reasons, some of the analysis on this website is based on the 25th Actuarial Report, published in 2010. In 2010, there was no surplus and no need to “control the narrative and hide things at will”. Since then, our Chief Actuary has skillfully buried the surplus in subsequent reports. Moreover, from 2016 to 2022, ten top Canadian actuaries have denied the surplus with vacuous arguments. Finally, our Chief Actuary’s four forecasts of all other issues combined that are related to the fund’s status have been virtually identical for the next 70 years.

The impact of our Chief Actuary’s deception is disastrous. For many Canadians, the CPP is their only savings for retirement. Roughly 75,000 pensioners are dying every year without seeing any of their fair share of the surplus, as much as $25,000 each. Two million seniors now live near the poverty line of $21,000 in income per year. Their deserved surplus payment would probably ten-tuple their discretionary income remaining after rent and day-to-day expenses have been paid.

Depriving just one senior of a deserved $25,000 is a tragedy. Depriving three million seniors of a deserved $44 billion is a catastrophe.

How can a respected country like Canada permit and condone such a tragedy? How can we deprive three million seniors of a deserved $44 billion and 14 million working Canadians of a deserved $126 billion?

The actuarial industry needs to gracefully accept their possible decline in job opportunities and not rob millions of Canadians of billions of deserved dollars. Consider other industries. Robots took factory workers’ jobs. ATM’s took tellers’ jobs. Online stores are taking retail workers’ jobs.

Regrettably, the impending decline of the actuarial industry is different. Actuaries, not management, report on the status of the CPP. If they all informally agree to deny an obvious, giant surplus, the news of the CPP’s surplus will never reach the public. Moreover, as explained elsewhere, the complicit Canadian media has never published anything on the CPP’s gigantic surplus and potential. Finally, the complicit financial industry is likely supplying funds to maintain the secrecy on the CPP’s surplus.

The actuarial industry does not want the news of the CPP’s surplus revealed for a second reason. The news would reveal that a deceptive Chief Actuary has hoodwinked Canadians for years. Millions of Canadians have a second pension fund, which holds as much as $2 million of their contributions. Members of these plans might demand much more scrutinized reporting and possibly a reduction in actuary’s fees.

There is more pension injustice in Canada. Almost all public sector employees, 25% of Canada’s work force, will retire with a pension that is as much as 70% of their final income. The average public sector worker income is $75,000 per year. Senior public sector workers near retirement would average an income much higher than $75,000. This means the average public sector pension is roughly $60,000 per year.

Because of employer matching, these generous $60,000 pensions are half paid for by by all Canadians. Meanwhile, the average CPP pension is only $8,600 per year. Compare a $60,000 pension, half paid for by all Canadians, to a CPP pension of $8,600, completely paid for by you and your employer. By denying the CPP’s irrefutable $257 billion surplus, our Chief Actuary is worsening this already unjust pension situation in Canada.

Beware of the pay-as-you-go argument

One top actuary tried to maintain the CPP has no surplus with the following argument.

There are two types of pension funds – those funded on an open group basis, known as a pay-as-you-go plan, and those funded on a closed group basis. The CPP is funded on an open group basis. This means some of your contributions are invested on your behalf and some of your contributions are used to pay pensioners.

The closed group pension plan is necessary for businesses because they can go bankrupt. If their fund is not 100% funded, pensioners, like those of Sears and Nortel, will be shortchanged. If a closed group fund is 100% funded at bankruptcy time, it will meet all pension obligations, if the specified investment return, roughly 6%, is achieved.

The open group basis is appropriate for the CPP because Canada will never go bankrupt. The CPP will always have a considerable number of employed contributors, now 14 million, and hence, considerable contributions to the CPP.

The Chief Actuary agrees. His most recent 30th Actuarial Report states on page 178:

“If the base Plan’s financial sustainability is to be measured based on its asset excess or shortfall, it should be done on an open group basis that reflects the partially funded nature of the base Plan, that is, its reliance on both future contributions and invested assets as means of financing its future expenditures.”

In 2021, the contributions totaled $56 billion, the pension payments totaled $49 billion, and the investment return was $74 billion, resulting in a net fund increase of $81 billion. Meanwhile, to fund our great grandchildren’s pensions, our Chief Actuary has stated he only needed a fund increase of $25 billion in 2021 .

This means the fund increased by $56 billion more than our Chief Actuary’s target for 2021 alone.

A debate could clear up confusion

Perhaps the most concrete proof of a cover-up by actuaries is their refusal to engage in a debate. CARP members, for example, would receive $1.7 billion from a CPP surplus distribution. Members are likely confused as they receive conflicting statements from me and CARP headquarters.

This confusion could be easily cleared up. Often CARP holds webinars. CARP could monitor a debate with me against any actuary. CARP has refused to arrange such a debate likely because the financial industry has “encouraged” them to never mention the CPP.

There is a second reason that CARP is not holding a debate. No actuary will come forward. No actuary wants to try to oppose the contents of this website. What actuary wants to claim the CPP does not have an irrefutable $257 billion surplus and 17 million Canadians do not deserve $10,000 each, on average. He would be very unpopular and likely judged as suspicious and foolish. Moreover, such a debate might lead to an increased scrutiny on all pension funds and all actuary’s income.

I have debated on the CPP for 40 hours with top actuary, Malcolm Hamilton. His lack of viable arguments proves that a surplus distribution is completely justified and the actuarial industry is denying the surplus to protect their at-risk industry,